Executive Summary: The Canadian iGaming Frontier

The Watershed Moment: 2026 marks Canada’s shift from a “pioneer” market (Ontario) to a multi-jurisdictional powerhouse. Alberta is transitioning from an exclusive government-operated model, currently PlayAlberta, to an open, regulated market for private operators, aiming to establish a competitive market that draws inspiration from Ontario’s framework.

The Pulse Check: This high-growth market is projected to reach CAD 1.9 billion in Gross Gaming Revenue (GGR) by 2030e. This growth is underpinned by a robust Compound Annual Growth Rate (CAGR) of 17% between 2024 and 2030e. The final deadline for operators to submit completed applications and pay all required fees to the Alberta Gaming, Liquor and Cannabis (AGLC) is July 13, 2026, with commercial operations expected to commence by late summer 2026.

The “Canada Paradox”: Understanding the Local Player

Demographic Nuances

Alberta presents a highly attractive target market with a population of approximately 5 million, 80% of whom are of legal gambling age (18+). The province boasts the highest economic output per capita in Canada, with a projected GDP of $72,000 in 2025.

A key strategic advantage for operators is Alberta’s high urban concentration: over 75% of the population resides within the Calgary-Edmonton Corridor. This density, combined with a 95% internet penetration rate and 97% smartphone adoption, creates a sophisticated, digitally mature audience. The market is overwhelmingly mobile-dominant, with 72% of total turnover generated via mobile channels and an impressive estimated average monthly spend per player of $210.

Product Preference Mapping

iCasino Dominance:

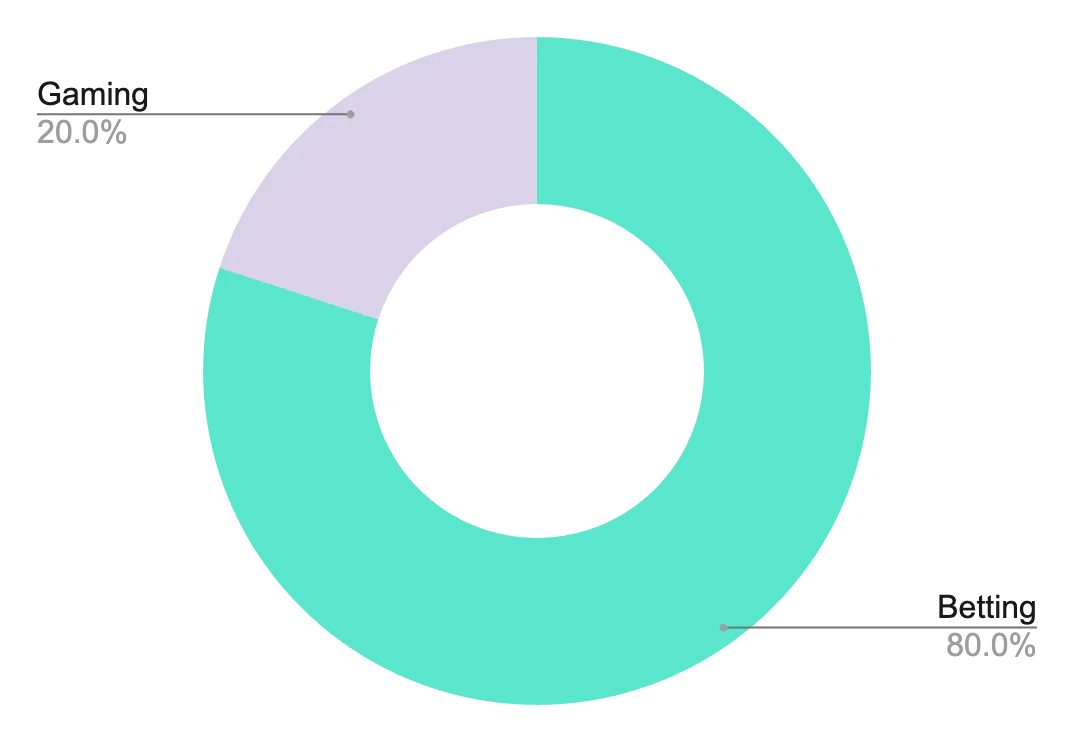

According to latest H2GC projections, the Alberta market is expected to be heavily weighted toward iCasino, which is forecast to represent nearly 80% of the total Gross Win compared to Sports Betting. Within the iCasino segment, Slots are projected to be the primary revenue driver at 81% of Gross Win, followed by Live Casino at 11%, RNG Casino at 6.5%, and Poker at approximately 1.5%.

The Sports DNA: Alberta Market Profile

Regional Wagering Trends (Benchmarked against Ontario): While Ontario provides a baseline, Alberta’s market is expected to reflect a more concentrated interest in specific regional rivalries. While Basketball (24%) and American Football (15%) will likely remain the highest volume drivers due to the high frequency of games, Ice Hockey is expected to over-index significantly in Alberta.

The “Battle of Alberta” Factor: With a deeply ingrained hockey culture and the fierce rivalry between the Edmonton Oilers and the Calgary Flames, Ice Hockey is anticipated to exceed Ontario’s 11% benchmark, serving as a primary driver for both player acquisition and peak wagering handle.

CFL & Western Football: In the Alberta market, the CFL (Stamps and Elks) maintains a stronger cultural foothold than in central Canada, providing a consistent wagering opportunity throughout the summer months.

Soccer (10%) & Baseball (11%): These categories are expected to mirror national trends, driven by major international events and the MLB season.

————————————————————————————————————-

Regulatory Restrictions: It is critical to note that Alberta’s regulatory framework aligns with Canadian integrity standards regarding amateur sports. Wagering on minor league sports—specifically the CHL (Western Hockey League / WHL)—is explicitly prohibited. For Alberta-based operators, this means popular regional teams like the Red Deer Rebels or Medicine Hat Tigers are excluded from the sportsbook offering to ensure the protection of amateur athletes.

————————————————————————————————————–

Payment preferences mapping: Canadian iGaming Payment Landscape

Nearly 99% of the Canadian population is banked, with approximately 77% having access to a credit card.

The Leaders (62%): Debit & Interac e-Transfer. These are no longer just preferences; they are utilities. With 46% of players prioritizing “instant payouts” above all else, Interac dominance is driven by the speed of the withdrawal, not just the ease of deposit.

Credit Cards (24%): Usage continues to slide from 30% as bank-side friction and regulatory scrutiny on “debt-funded” play increase. Credit is increasingly viewed as an “emergency” or secondary method.

Digital Wallets (28%): Now a “Daily Habit” for VIPs. Among high-frequency bettors (5+ bets/week), usage spikes to 41%. Wallets act as the primary liquidity bridge for players managing multiple sportsbook accounts during major events like the 2026 World Cup.

eCash & Vouchers (17%): Adoption has nearly tripled since 2023. It has become the primary entry point for 10% of new players and serves as a critical Responsible Gaming (RG) tool for those wanting physical “hard limits” on their spending.

Local Payment Methods (LPMs): Since Canada’s Real-Time Rail (RTR) rollout, 19% of players explicitly scan a cashier for “Canadian-native” logos. Failure to provide a localized, frictionless experience results in an 88% player abandonment rate after the first failed transaction.

In 2026, the competitive advantage has shifted from what methods you offer to how fast they settle. If your payout isn’t instant, your player is gone.

The Regulatory Pillars (The “How-To” of Compliance)

The Provincial Quilt: The Alberta market, regulated by the AGLC and the Alberta iGaming Corporation (AiGC), is transitioning to an open, competitive model, moving away from its government-only PlayAlberta platform. This legislation, enabled by Bill 16 (passed May 2024), aims to establish a framework inspired by Ontario’s open market success.

The Alberta Blueprint (July 2026):

Licensing Framework: Operators are required to pay a one-time C$50,000 application fee and an annual C$150,000 registration fee. A license supplier is also required under the new regulation.

Competitive Tax Framework:

The province uses a tiered deduction model on Gross Gaming Revenue (GGR). While the base rate is 20%, mandatory contributions for social and community impact bring the actual cost to operators up to 22.4%.

Total Financial Commitment: 22.4% (often rounded to 23%).

Breakdown of Allocations:

20%: Provincial tax (Base rate).

2%: Support for Indigenous Communities (First Nations).

1%: Responsible gambling and player safety (Social Responsibility).

The “New Rules” of Engagement: Prohibited Games and Categories include: minor league sports in Canada (such as the CHL), bets on past events, animal cruelty, financial markets and instruments, synthetic lottery products or lottery outcomes, political events, and any bets deemed objectionable or likely to result in excessive losses.

Player Security and Geolocation

Compliance is mandatory for the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA) and FINTRAC guidelines. Operators must verify the players full name, date of birth, and FINTRAC-compliant physical address upon registration. To ensure geographical restrictions are met, gaming systems must continually monitor and re-verify player location to ensure play occurs exclusively within Alberta, actively blocking evasion methods like VPNs.

Responsible Gaming and Prohibitions

The province mandates robust Responsible Gaming (RG) measures, including a centralized AGLC-managed Self-Exclusion system. Operators must offer tools for players to set mandatory limits on deposits, losses, and session time. Any request to increase or relax a limit requires a mandatory 24-hour cooling-off period. Furthermore, operators are required to proactively monitor player behavior for potential harm and intervene immediately.234

Advertising must include an RG message, and self-excluded players must be blocked from all marketing. The AGLC explicitly prohibits certain game mechanics, such as Auto-Play and Multi-Play, and any misleading game designs.

Why GiG?

GiG is uniquely positioned to support operators through the Alberta expansion by combining proven technology with local regulatory expertise:

Official Alberta Licensure: GiG has officially secured its supplier license from the Alberta regulator, solidifying its status as a fully compliant and authorized technology partner. This ensures a seamless and fully vetted transition for operators entering the province.

Proven Ontario Blueprint: Leveraging a platform already successful in Ontario’s competitive landscape, GiG’s compliance and localization stacks are engineered to meet the strict identity verification and advertising standards expected in Alberta.

Accelerated Time-to-Market: With extensive experience across North American jurisdictions, GiG enables operators to navigate complex regulatory environments with confidence, significantly reducing the friction of market entry.

Technology Partner of Choice: Our infrastructure provides the flexibility and control required for Tier-1 operators to scale their operations according to their specific strategic priorities and growth targets.

Commitment to Sustainable Growth: GiG combines robust, partner-led technology with a focus on long-term success, ensuring that performance and player protection remain at the core of every operation.